Welcome to the 12th edition of Wednesday Wisdoms by EdGenie!

Every Wednesday I send out actionable tips, tricks and real-world application insights from my 13-year experience coaching students to achieve As and A* in their Economics and Business A Levels.

Jump to Section:

Working Hard, But it's Hardly Working?

Cost of National Debt hits 20-Year High

Infographic of the Week

Chart of the Week

Macroeconomic Data

Working hard, but it's hardly working?

Hi Genies! 🌟

So, you’ve hit the books hard, but those A-level Economics grades aren’t mirroring your effort.

Frustrating?

Absolutely.

But we’re in this together, and today let's dig a little deeper into “why” you may be struggling to secure the top grades

📘 Maybe the Guidance Isn't Quite Right:

The advice you’re getting might be solid but think - is it aligning with the exam board’s demands? Remember that 25-marker on the impact of inflation? We didn’t just need definitions; it was all about depth, context, and a sprinkling of real-world applications, like considering the recent economic climate or governmental policies.

🦜 Rote Learning’s a Sneaky Trap:

Sure, you know your definitions. For instance, you can describe 'monetary policy' in your sleep. But can you argue how effective it’s been in recent years in the UK, especially during economic downturns? It’s that next step of applying and arguing that makes the difference.

📈 Trapped in the Theoretical:

Yes, theory’s vital but remember that time we discussed interest rates and you knew all the facts? The exam will ask you to apply that to, perhaps, the impact on consumers and businesses during a specific economic event, like the pandemic or inflation crisis. It’s applying those facts that will snag those marks.

🚀 Misfiring on Priorities:

Easy to do - sticking to what you know and like. But, did you know that a stunning in-depth evaluation can elevate a ‘meh’ essay to a star-studded one? For example, don’t just stop at explaining fiscal policy. Dive deep into the nuances - like considering short-term vs. long-term impacts or societal implications.

Conclusion

Alright, let’s keep it real. Economics is no walk in the park, and we all know it.

Those higher marks won’t just fall into our laps, and the road to acing those exams? It needs a solid, smart plan. So, let’s knuckle down, figure this out, and turn those tricky theories into top grades. It's not just about hitting the books harder, but smarter. Together, we’re gonna get to grips with this stuff, cut through the jargon, and make sure those exams know exactly who they’re dealing with. Are you with me?

📈 Key Figures: - 30-year bond rate now stands at 5.05%. - The UK's towering national debt: a whopping £2.59 trillion. - Rising rates mean an additional cost of £23 billion.

🔍 Inside The Government's Decisions:

Chancellor Jeremy Hunt braces for the autumn statement on 22 November.Spoiler Alert: No tax cuts this November.Rising debt costs could mean critical decisions on where to allocate funds.

💰 Bonds & Borrowing Explained:

How does the UK government borrow? By selling bonds promising future payments.The trust factor: UK's bonds, known as "gilts", are seen as a safe bet.Main Players: Financial institutions at home and across borders.

🏛 Bank of England's Hand:

Massive bond purchases via a strategy called "quantitative easing" to prop up the economy.

⚖️ The Balancing Act:

With higher debt servicing costs, there might be tighter budgets for public services.Workers' demands: A pay that resonates with the cost of living.A walk down memory lane: Today's debt is more than double from the 1980s to the pre-2008 financial crisis era.

🌍 A Global Glimpse:

The ripple effect: The US, Germany, and Italy face escalating borrowing costs.Central Banks' Stance: Prepare for interest rates to stay "higher for longer".

🤔 Economists Weigh In:

The Dilemma:Is the UK government digging too deep a hole?Or, is this borrowing a path to a prosperous future, promising more tax revenue in the end?

🔮 Looking Ahead:

An ageing cloud on the horizon? The Office for Budget Responsibility (OBR) shares a future where an ageing population could mean decreased tax and heightened pension expenses.

A Level Economics Questions:

Q: Explain the impact of a rise in interest rates on government borrowing, using the specific example of the UK's 30-year bond rate rising to 5.05%. A: A rise in interest rates increases the cost of borrowing for the government. Specifically, when the UK's 30-year bond rate rose to 5.05%, it meant that for every bond issued, the government would have to pay a higher amount of interest over the bond's lifetime. This can lead to an increase in the cost of servicing the national debt, as indicated by the additional £23 billion the UK government would need to set aside for interest payments. Higher borrowing costs can also influence government decisions on spending, potentially leading to reduced public expenditure or the need to raise taxes to cover the interest payments.

Q: Discuss the potential implications for public services, such as healthcare and education, when the government has to allocate more funds for debt servicing.

A: When the government has to allocate more funds for debt servicing, it may result in reduced allocation for public services like healthcare and education. This could lead to cuts in these sectors, possibly resulting in fewer services being offered, delays in infrastructure upgrades, or even potential staff reductions. For instance, with workers in key industries demanding pay rises to match the cost of living, there may be added pressure on the budget. Such reductions can have long-term implications on the quality of public services and the overall well-being of the population.

Q: Using the example of the Bank of England's quantitative easing, explain how central banks can influence the demand for government bonds.

A: Quantitative easing (QE) is a process where central banks purchase government bonds to inject money directly into the economy. In the case of the Bank of England, it bought hundreds of billions of pounds' worth of government bonds. This action increases the demand for these bonds, which can lead to a rise in bond prices and a fall in their yield (or interest rate). By doing so, QE can help lower the interest rates at which the government borrows, thereby reducing its borrowing costs.

Q: Analyse the potential challenges an ageing population presents to a country's fiscal policy, drawing on the warnings from the Office for Budget Responsibility (OBR).

A: An ageing population can pose significant challenges to a country's fiscal policy. As the proportion of the working-age population decreases:

Tax Revenues: There's a potential decrease in tax revenues as fewer people are in the workforce, leading to less income tax collection.

Pension and Healthcare Costs: Governments may face higher pension obligations and healthcare costs, as older populations typically require more medical care.

Dependency Ratio: A higher old-age dependency ratio means fewer workers supporting a larger retired population, which can strain social security systems.

Economic Growth: Potential slowdown in economic growth due to reduced labour force participation.

The OBR's warning underscores these challenges, emphasizing that public debt could soar as the ageing trend intensifies, thereby necessitating revisions in fiscal policies to maintain economic stability.

Possible A Level Economics 25 Marker Question

Evaluate the potential short-term and long-term economic impacts of rising government borrowing costs on public services, economic growth, and overall fiscal stability. Use evidence from the article and your own knowledge to support your arguments.

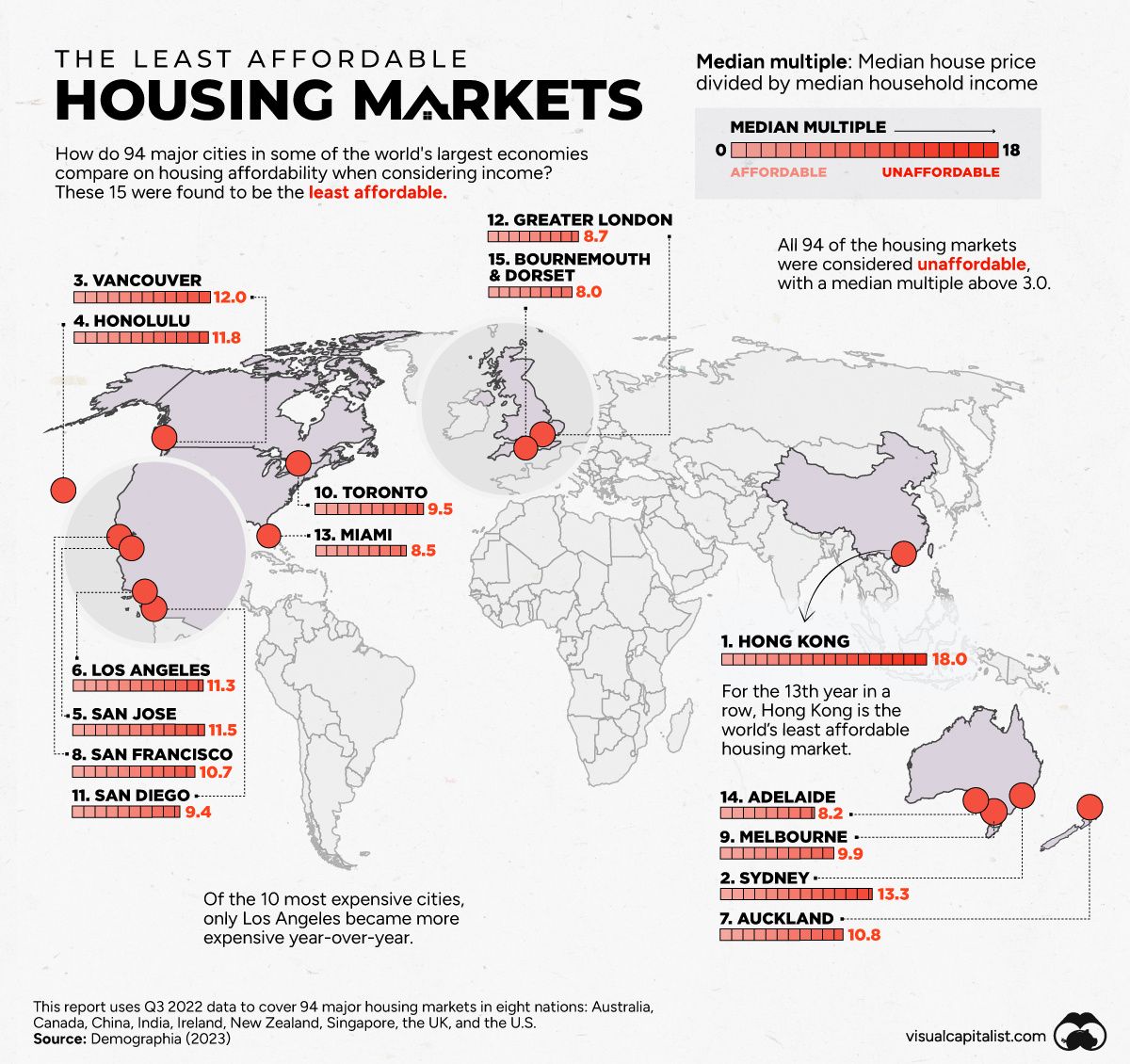

Infographic of the Week

The Least Affordable Housing Markets

In 2023, based on data from Demographia, none of the 94 major cities across eight countries, including Australia, Canada, China (Hong Kong), Ireland, New Zealand, Singapore, the UK, and the U.S., were deemed "affordable" in terms of housing. Hong Kong tops the list with a housing median multiple of 18.8, indicating extreme unaffordability, followed by cities like Sydney, Vancouver, and Honolulu. Conversely, the most affordable cities, all located in North America, include Pittsburgh, Rochester, and Cleveland. The high housing costs in major cities may drive potential residents to consider more affordable alternatives for financial viability.

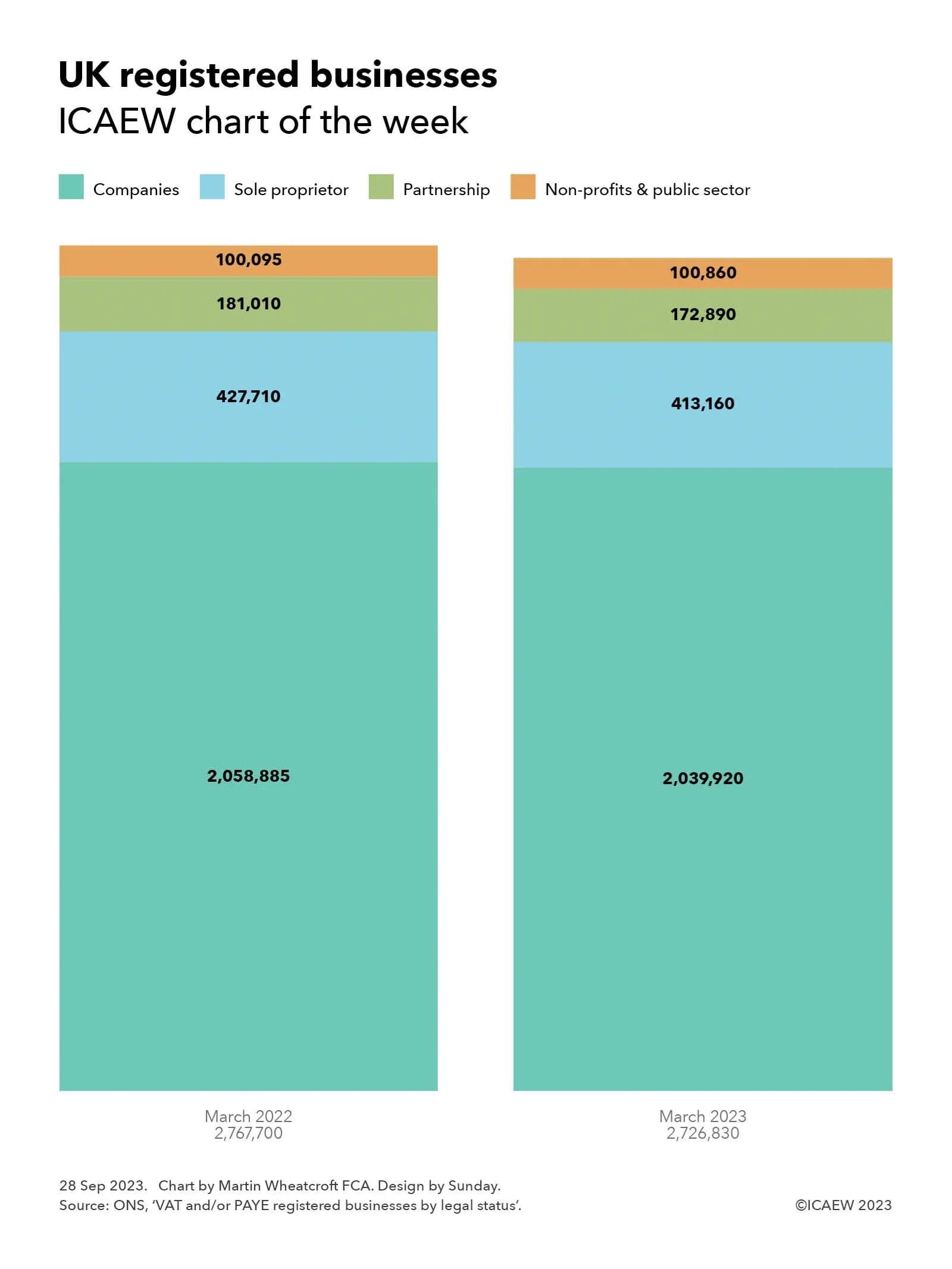

Chart of the Week

UK Registered Businesses

In the year leading up to March 2023, the UK saw a 1.5% decline in VAT- and PAYE-registered businesses, as reported by the Office for National Statistics (ONS). While the total number decreased from 2,767,700 to 2,726,830, the breakdown reveals a 0.9% drop in registered companies, 3.4% in sole proprietorships, and 4.5% in partnerships. In contrast, non-profit organizations, mutual associations, and public sector entities experienced a 0.8% increase. Although not included in the chart, approximately 2.8 million unregistered businesses exist, primarily comprising self-employed individuals or those below the VAT threshold. The decrease in business numbers is attributed to pandemic support which delayed typical business closures and challenges such as the energy crisis and rising living costs potentially threatening further businesses in 2023/24.

Macroeconomic Data

Whenever you're ready there is one way I can help you.

If you or your child are looking to Boost your A level Economics Grades in under 30 days, I'd recommend starting with an all-in-one support network where you get 24/7 access to a SuperTutor:

→ Join EdGenie 🧞♂️: Transform your A-Level Economics essays and exam marks (genuinely) with our comprehensive on-demand learning platform. This carefully curated course blends engaging content with effective exam techniques, the same ones that have empowered over 1,000 of my students to achieve an A or A* over the last 13 years.

A huge thanks for hopping on board EdGenie's Wednesday Wisdoms newsletter!

I'm Emre, and I've got a big goal - to make A* education accessible to all A-level students.

And it Starts With You!

Emre Aksahin

Chief Learning Officer at Edgenie

Join EdGenie 🧞♂️

Unlock Full Access to Examinable Questions and Answers, Plus: